The Annual Lock-In Strategy

- Christopher Krolak

- 2 hours ago

- 6 min read

Why More Retirees Are Protecting Their Gains Instead of Giving Them Back

Imagine this.

Your retirement portfolio has a fantastic year. The market performs well, and your

account grows by 15%.

Then the following year, the market falls 20%.

How much of last year's gain do you still have?

For many investors, the answer is very little—or none at all.

That's because traditional investment portfolios rise and fall with the market. Gains aren't permanent until you sell, and even then, future market declines can erase years of progress.

But what if there were another way?

What if, instead of worrying about giving back years of growth during the next market correction, you could automatically lock in your gains every year?

This concept is known as The Annual Lock-In Strategy, and for many pre-retirees and retirees, it's changing the way they think about protecting their retirement savings.

Retirement Changes the Conversation

When you're 35 years old, market declines are usually viewed as temporary setbacks.

You have years—even decades—to recover.

But retirement changes the equation.

Now you're asking questions like:

Will my money last?

What happens if the market drops right after I retire?

Can I continue taking income without selling investments at a loss?

How much risk do I really need?

At this stage of life, protecting what you've already earned often becomes just as important as earning more.

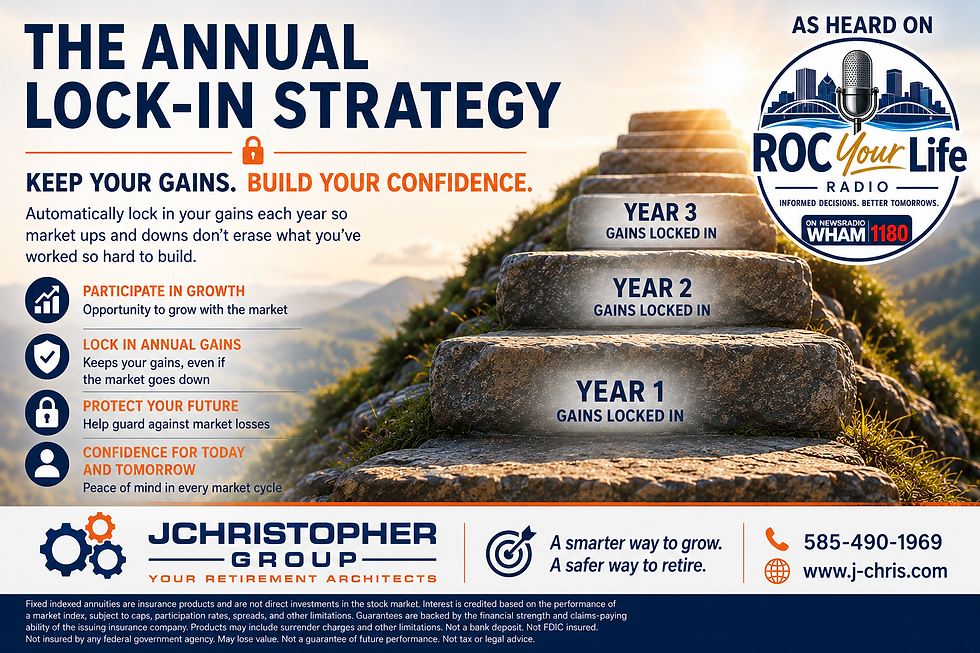

What Is an Annual Lock-In Strategy?

An annual lock-in is a feature available in many fixed indexed annuities.

Here's how it works.

Each year, your account has the opportunity to earn interest based on the performance of a market index, subject to the terms of the contract, such as participation rates, caps, or spreads.

At the end of each crediting period:

Any interest you've earned is credited to your account.

That interest becomes part of your protected account value.

If the market declines the following year, those previously credited gains are not lost because of market performance.

Think of it like climbing a staircase.

Every step you climb becomes your new starting point.

You don't slide back down simply because the market has a bad year.

That's very different from traditional market investing, where account values can fluctuate significantly from one year to the next.

"I've Heard Annuities Are Bad..."

If you've been researching retirement strategies for any length of time, you've probably heard someone say, "Stay away from annuities."

It's one of the most common statements I hear from new clients.

The truth is, "annuity" isn't a single product.

It's a broad category of insurance contracts, much like the word "vehicle" could describe a sports car, an SUV, or a pickup truck. They all serve different purposes.

Some annuities—particularly certain older variable annuities—earned a poor reputation because of high fees, complicated features, and exposure to stock market losses. In many cases, those criticisms were justified.

But that's only one type of annuity.

Fixed indexed annuities were designed for a different purpose.

Rather than trying to outperform the stock market, they're designed to help protect your principal from market losses while still providing the opportunity to earn interest based on market performance.

Like any financial strategy, they aren't appropriate for everyone. But dismissing every annuity because of experiences with one type is a little like saying all investments are bad because someone lost money buying a single stock.

The better question isn't:

"Are annuities good or bad?"

The better question is:

"Is this particular strategy appropriate for my retirement goals?"

See Whether an Annual Lock-In Strategy Fits Your Retirement Plan

If you've never had someone explain how today's fixed indexed annuities work—or how they differ from the products that gave annuities a mixed reputation—you owe it to yourself to learn more.

During a complimentary retirement strategy review, we'll compare your current portfolio with alternative approaches, explain the advantages and tradeoffs of each, and answer your questions in plain English.

No pressure. No obligation. Just education so you can make an informed decision.

📞 Call JChristopher Group at 585-490-1969🌐 Visit www.j-chris.com

A Simple Example

Let's assume you begin with $200,000.

Year One

Interest credited: +10%

Account Value:

$220,000

That gain is now locked in.

Year Two

Interest credited: +8%

Account Value:

$237,600

Again, those gains become protected.

Year Three

The market experiences a significant decline.

Instead of losing 20%, 25%, or even 30%, your interest credited for that year may simply be 0%, depending on your contract.

Your account remains:

$237,600

You begin the following year from your new high-water mark instead of trying to recover from a substantial loss.

Why Avoiding Losses Matters

One of the biggest misconceptions in investing is that recovering from losses is easy.

It's not.

Market Loss | Gain Needed to Recover |

10% | 11% |

20% | 25% |

30% | 43% |

40% | 67% |

50% | 100% |

The larger the loss, the harder it becomes to get back to where you started.

That's why protecting gains can be just as valuable as earning them.

Retirement Isn't About Winning the Market

Many investors spend decades trying to maximize returns.

But retirement isn't an investment competition.

It's about creating a lifestyle.

Your goal isn't necessarily to have the highest return every year.

Your goal is to have enough income, enough growth, and enough stability to confidently enjoy retirement without worrying about every market correction.

Sometimes earning a little less during the market's strongest years is a worthwhile tradeoff if it helps avoid devastating losses during the weakest years.

Confidence Has Value Too

We've all watched the headlines during difficult markets.

Investors become nervous.

Some delay retirement.

Some stop spending.

Others sell after the market has already declined, locking in losses that might have been temporary.

Knowing your previously credited gains cannot disappear because of market performance provides something many retirees value just as much as returns:

Confidence.

Confidence to stay the course.

Confidence to continue enjoying retirement.

Confidence that a bad year in the market doesn't necessarily have to become a bad year for your retirement plan.

A Different Way to Think About Retirement

For most of your working years, you probably asked one question:

"How much can I make?"

As retirement approaches, a more important question often becomes:

"How much of what I've already earned can I keep?"

That's exactly what the Annual Lock-In Strategy is designed to address.

It doesn't eliminate every financial risk, and it isn't appropriate for every investor. But for many pre-retirees and retirees, it offers an opportunity to participate in market-linked growth while protecting previously credited gains from future market declines.

That's a conversation worth having.

Ready for a Second Opinion?

At JChristopher Group, we believe every dollar should have a purpose.

Some dollars are meant to generate dependable income.

Some are meant to provide long-term growth.

And some are meant to provide stability, so you don't have to make emotional financial decisions during periods of market volatility.

If you're within five to ten years of retirement—or already retired—and you'd like to see whether an Annual Lock-In Strategy could strengthen your retirement plan, we'd be happy to help.

During your complimentary retirement strategy review, we'll:

Review your current portfolio.

Identify where you're taking unnecessary risk.

Explain how annual lock-in strategies work.

Compare your current approach with alternative retirement strategies.

Help you determine whether protected growth fits your financial goals.

There is no cost, no obligation, and no sales pressure—just an opportunity to gain clarity and confidence about your retirement.

Call JChristopher Group today at 585-490-1969 or Visit us online at www.j-chris.com

Because in retirement, it's not just about making money.

It's about keeping the money you've already earned.

Disclosure

Fixed indexed annuities are insurance products and are not direct investments in the stock market. Interest is credited based on the performance of a market index, subject to contract terms that may include participation rates, caps, spreads, and other limitations. Principal and previously credited interest are generally protected from market losses when held according to the terms of the contract. Guarantees are backed solely by the financial strength and claims-paying ability of the issuing insurance company. These products may include surrender charges, withdrawal limitations, and other restrictions and may not be appropriate for every individual. This article is provided for educational purposes only and should not be considered investment, tax, or legal advice. Please consult your financial, tax, or legal advisor regarding your specific situation.

Comments